Major BC Breweries Lead the Way in Declining Sales

Over 6% year-over-year declines in litre and net $ sales from BC major breweries driving overall downward trend

- Major BC breweries are driving the overall decline in beer sales, with ~6–7% YoY drops in both litres and net $ (Jan–Sep 2025).

- Regional BC breweries are the only consistent bright spot, showing modest growth in both volume and sales.

- BC microbreweries remain negative but the rate of decline is easing, hinting at a possible bottoming out.

This is a follow-up to BC Beer Sales Show Continued Multi-Year Decline in 2025 Data. It draws on data published by the BC Liquor Distribution Board in its latest quarterly Liquor Market Review, using the interactive dashboards on BCBeer.ca. To keep comparisons consistent, I focus on the first nine months of each year (Jan thru Sep), given data available at the time of writing.

This article focuses on recent sales trends for BC Beer Producers.

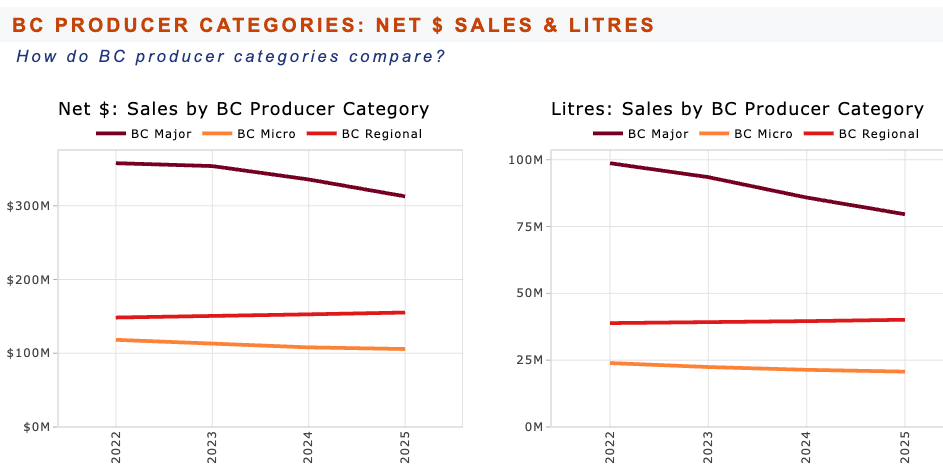

- BC producers make up ~80% of BC beer litre sales.

- 4.4% decline in litres sold from BC producers during Jan-Sep of 2025 compared to Jan-Sep 2024

- drop of 6.4 million litres to 140.4 million litres, accounting for most all of the 7.7 million litre overall decline.

Let’s a take a look at what is happening by subcategory:

- BC Major ‘Commercial’ producers

- BC Regional producers

- BC ‘Micro’ producers - essentially equivalent to craft beer

BC Major Producers are Driving the Declines

Major breweries dominate volume and are driving the downward trend, as can be seen in net $ sales (left) but even more predominantly in litre sales (right).

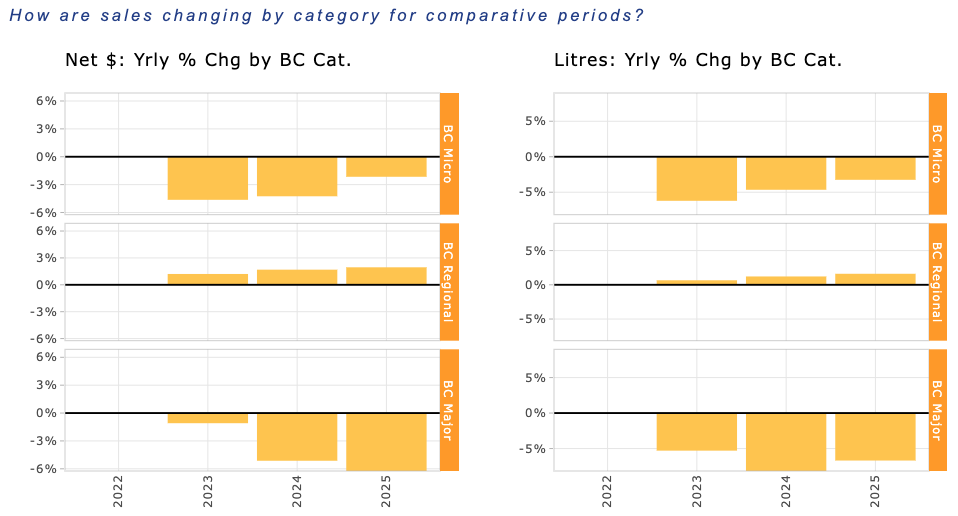

Percentage Changes Highlight Differences by Category

BC Major Breweries taking the hit

- 6.7% decline in litres (although less severe than the 2024 vs 2023 drop).

- 6.2% drop in net $ and falling - suggesting price drops intended to spur sales.

BC Regional breweries growing slowly

- modest but steady growth, both $ and litres makes this the winning category.

BC Micro Breweries negative but trending up

- net $ and litres in negative territory, but declines are decreasing, possibly indicating bottoming-out and maybe eventual return to growth.

- down 3.3% in litres and -2.2% for net $ suggesting ability to hold or even raise prices.

Summary tables

Tables below for exact figures.

| Net $ Sales: YoY Change by Category | |||

|---|---|---|---|

| First 9 months, 2023-2025 | |||

| 2023 | 2024 | 2025 | |

| BC Major | −1.1% | −5.1% | −6.2% |

| BC Micro | −4.6% | −4.3% | −2.2% |

| BC Regional | 1.2% | 1.7% | 2.0% |

| Litres: YoY Change by Category | |||

|---|---|---|---|

| First 9 months, 2023-2025 | |||

| 2023 | 2024 | 2025 | |

| BC Major | −5.3% | −8.2% | −6.7% |

| BC Micro | −6.2% | −4.7% | −3.3% |

| BC Regional | 0.7% | 1.2% | 1.6% |

Conclusion

- In short: the majors are pulling the market down, while regional producers are the only bright spot.

- BC microbreweries still losing sales but may be in a turn-around toward growth.

Up Next: Dec 31, 2025 update

Next update will cover Q4 2025 once next BC Liquor Market Review is released. We’ll be able to see full-year trends at that point.

More info on BC Beer Sales…

As always, for more info, check out the full suite of BC Sales Stats dashboards available on this site.